According to the Asian Development Outlook – July 2025 by the Asian Development Bank (ADB), the economic outlook for Southeast Asia and Vietnam is under increasing pressure due to a more complex external environment, particularly trade tensions and new U.S. tariff policies.

Southeast Asia: Growth Forecast Revised Downward

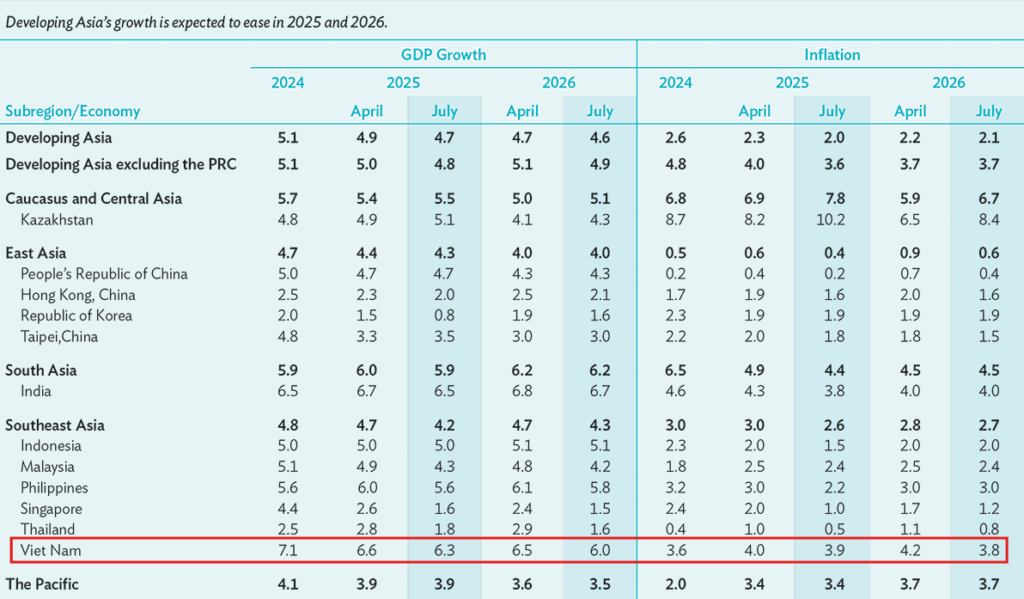

Southeast Asia saw the sharpest downward revision in growth forecasts among all developing Asian subregions. ADB has lowered the region’s GDP growth forecast to 4.2% for 2025 and 4.3% for 2026, down 0.2 and 0.3 percentage points from the April projections.

The main reasons are global trade instability, weaker external conditions, and declining investor and consumer sentiment. Although export growth was recorded in Q1/2025 due to frontloading ahead of tariff imposition, the outlook for most regional economies has been revised downward:

- Malaysia: GDP forecast lowered to 4.3% (2025) and 4.2% (2026) due to weaker trade and investment outlook.

- Philippines: revised to 5.6% (2025) and 5.8% (2026) amid rising external risks.

- Singapore and Thailand: affected by weakened global demand, trade tensions, and slow tourism recovery.

Regional inflation is also expected to continue its downward trend, averaging 2.6% in 2025 and 2.8% in 2026, mainly due to stable energy and food prices, weak consumption, and stronger currencies. Some central banks have cut interest rates to support growth.

Vietnam: Recovery Continues but Faces Tariff Pressure

Vietnam is expected to maintain its recovery momentum in 2025 and 2026, but growth projections have been revised downward due to the impact of new U.S. tariffs. ADB lowered its GDP forecast to 6.3% in 2025 and 6.0% in 2026, down from 6.6% and 6.5% in the April outlook.

This adjustment stems from a bilateral trade agreement between Vietnam and the United States announced in early July 2025, under which the U.S. will gradually impose higher import tariffs on Vietnamese exports. This is expected to affect exports starting in the second half of 2025 and extend into 2026. At the same time, Vietnam’s manufacturing PMI has declined since late 2024, indicating a slowdown in production.

However, there are still positive signals for Vietnam in the first half of 2025:

- Sharp increase in trade ahead of tariff implementation.

- Foreign direct investment registration up by 32.6%, and disbursement up 8.1% year-on-year.

- Public investment disbursement reached 24.3% of the annual plan, the highest rate since 2018.

Inflation in Vietnam is projected to remain below 4% through 2026, providing room for macroeconomic stability and more flexible policy responses going forward.

Latest Posts

- Vietnam’s 11.7% Growth Target for H2 2026: A Major Opportunity, But Businesses Cannot Ignore Risks

- AI Is an Amplifier: Need to Review Governance System Before Adopting

- Viet Nam amid a Slowing Global Economy: Growth and Challenges

- Vietnam’s Economy in May 2026: Strong Growth in a Phase of Capital Quality Testing

- What Should Businesses Do in a More Challenging Market and a More Selective Capital Environment?